About MUJIThree Principles in ManufacturingAbout the Advisory BoardProduct ArchivesArchivesNewsOur BusinessesMUJI BusinessesProduct Development and RetailAccommodationsFood ServicesCommunity EngagementArchitecture and Spatial DesignOther BusinessesIDÉE BusinessesCorporate InformationMessage from the PresidentOur Corporate PurposeThe Journey of Ryohin KeikakuCorporate ProfileLocationManagementGroup CompaniesThe Ryohin Keikaku Group by the NumbersOur HistoryStore Opening DataAwardsArchivesArticlesInvestor RelationsIR NewsLatest MaterialsIR CalendarMessage to Individual InvestorsIf you Become a Shareholder...EventsShareholders Special Benefit ProgramsCompany InformationManagement PolicyCorporate GovernanceIR PolicyFinancial InformationSummary of Financial ResultsFinancial HighlightsMonthly Sales FlashCredit Ratings and BondsStock InformationBasic Stock InformationStock Price InformationShareholder StatusGeneral Meeting of ShareholdersDividends / Shareholder ReturnsAnalyst CoverageArticles of Incorporation電子公告Tax PolicyIR LibraryLatest IR MaterialsConsolidated Financial ResultsData BookFinancial Results BriefingSecurities ReportConvocation Notice and Reports of Shareholders MeetingIntegrated ReportIR Briefing SessionDisclaimerIR registrationIR FAQContact us regarding IRSustainabilityIntegrated ReportESG DataMessage from the PresidentRyohin Keikaku and SustainabilityBasic Policy and ESG Management StructureMaterial Issues and IndicatorsOur PoliciesOur Approach to Product DevelopmentTopicsSustainability NewsRespect for the EnvironmentEnvironmental ManagementResponse to Climate ChangeResource CirculationThe "Design for Circularity" Product SeriesWaste ManagementWater Resource ManagementChemical ManagementBiodiversityRaw Material ProcurementEngagement with SocietyRespect for Human RightsHuman Rights Policy and Internal FrameworkHuman Rights Due DiligenceGrievance MechanismRespect for ColleaguesHuman Capital StrategyWorkplace Safety and Employee HealthMaintaining a Positive Work EnvironmentRespect for DiversityHuman Resource Development and Career DevelopmentCo-Owned Management and EngagementBasic Policy on Harassment from CustomersSupply Chain ManagementCode of Conduct for Production PartnersMonitoring Production PartnersList of Production PartnersSupplier HotlineIndirect ProcurementCustomer Safety and Peace of MindCustomer FeedbackQuality and SafetyFood-Related Responsibilities to CustomersAs a Community Center Activities at StoresRegions and CommunitiesSocial Impact AssessmentGovernancePublic Interest and People-Centered ManagementStakeholder EngagementCorporate Governance Policy and SystemAssessment of Effectiveness of the Board of DirectorsInternal ControlComplianceRisk ManagementInformation Security and Protection of Personal InformationParticipating in InitiativesExternal EvaluationsDonations and AssistanceTopRecruitOnline StoreContactメインナビゲーションメニューを閉じるメニューを開くAbout MUJIThree Principles in ManufacturingAbout the Advisory BoardProduct ArchivesArchivesNewsOur BusinessesMUJI BusinessesProduct Development and RetailAccommodationsFood ServicesCommunity EngagementArchitecture and Spatial DesignOther BusinessesIDÉE BusinessesCorporate InformationMessage from the PresidentOur Corporate PurposeThe Journey of Ryohin KeikakuCorporate ProfileLocationManagementGroup CompaniesThe Ryohin Keikaku Group by the NumbersOur HistoryStore Opening DataAwardsArchivesArticlesInvestor RelationsIR NewsLatest MaterialsIR CalendarMessage to Individual InvestorsIf you Become a Shareholder...EventsShareholders Special Benefit ProgramsCompany InformationManagement PolicyCorporate GovernanceIR PolicyFinancial InformationSummary of Financial ResultsFinancial HighlightsMonthly Sales FlashCredit Ratings and BondsStock InformationBasic Stock InformationStock Price InformationShareholder StatusGeneral Meeting of ShareholdersDividends / Shareholder ReturnsAnalyst CoverageArticles of Incorporation電子公告Tax PolicyIR LibraryLatest IR MaterialsConsolidated Financial ResultsData BookFinancial Results BriefingSecurities ReportConvocation Notice and Reports of Shareholders MeetingIntegrated ReportIR Briefing SessionDisclaimerIR registrationIR FAQContact us regarding IRSustainabilityIntegrated ReportESG DataMessage from the PresidentRyohin Keikaku and SustainabilityBasic Policy and ESG Management StructureMaterial Issues and IndicatorsOur PoliciesOur Approach to Product DevelopmentTopicsSustainability NewsRespect for the EnvironmentEnvironmental ManagementResponse to Climate ChangeResource CirculationThe "Design for Circularity" Product SeriesWaste ManagementWater Resource ManagementChemical ManagementBiodiversityRaw Material ProcurementEngagement with SocietyRespect for Human RightsHuman Rights Policy and Internal FrameworkHuman Rights Due DiligenceGrievance MechanismRespect for ColleaguesHuman Capital StrategyWorkplace Safety and Employee HealthMaintaining a Positive Work EnvironmentRespect for DiversityHuman Resource Development and Career DevelopmentCo-Owned Management and EngagementBasic Policy on Harassment from CustomersSupply Chain ManagementCode of Conduct for Production PartnersMonitoring Production PartnersList of Production PartnersSupplier HotlineIndirect ProcurementCustomer Safety and Peace of MindCustomer FeedbackQuality and SafetyFood-Related Responsibilities to CustomersAs a Community Center Activities at StoresRegions and CommunitiesSocial Impact AssessmentGovernancePublic Interest and People-Centered ManagementStakeholder EngagementCorporate Governance Policy and SystemAssessment of Effectiveness of the Board of DirectorsInternal ControlComplianceRisk ManagementInformation Security and Protection of Personal InformationParticipating in InitiativesExternal EvaluationsDonations and AssistanceTopRecruitOnline StoreContactメインナビゲーションメニューを閉じるメニューを開く

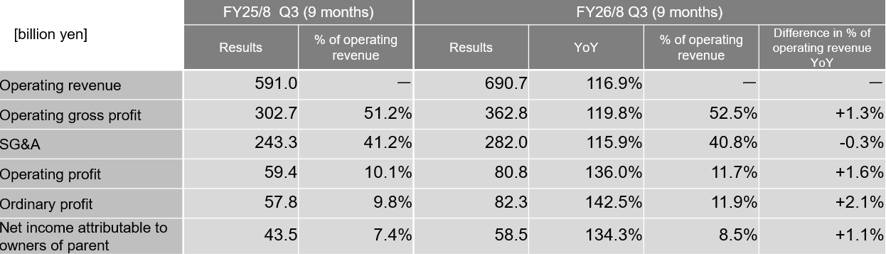

Executive Summary: With continued improvement in earnings, operating revenue and profits at all levels reached record highs.

Operating revenue increased by 16.9% YoY to 690.7 billion yen due to an increase in the number of stores both in Japan business and overseas business, as well as growth in sales in overseas business particularly.

Gross profit margin improved by 1.3pp YoY to 52.5%, driven by product cost reductions achieved through strengthening in-house production and an improvement in discount rate.

SG&A/revenue ratio improved by 0.3pp YoY to 40.8%, driven by sales growth.

As a result, operating profit increased significantly by 36.0% YoY to 80.8 billion yen. Operating profit margin improved by 1.6pp YoY to 11.7%.

Segment Results for FY2026/8 (9 months)

Japan business: Operating profit margin increased due to improvement in gross profit margin.

Operating revenue was 391.1 billion yen (108.9% YoY) and operating profit was 51.1 billion yen (123.9% YoY), resulting in increased revenue and profit.

Operating revenue maintained steady growth, driven by promotional campaigns such as “MUJI Week”, “MUJI Good Price Festival” and “Good Point Week”.

Following recovery from suspension, EC sales showed a recovery trend entering Q3, with LFL store + EC sales for Q3 (9 months) reaching 102.0% YoY.

Gross profit margin improved due to product cost reductions achieved through strengthening in-house production and an improvement in discount rate, and operating profit margin improved by 1.6pp YoY to 13.1%.

East Asia business: Sales performed well across all regions, with operating profit margin exceeding 21%.

Operating revenue was 212.8 billion yen (129.3% YoY) and operating profit was 45.4 billion yen (139.6% YoY), resulting in increased revenue and profit.

Operating revenue increased due to strong sales at LFL stores. LFL store + EC sales for Q3 (9 months) were 114.9% YoY.

Operating profit increased due to an improvement in SG&A/revenue ratio alongside sales growth, in addition to improvements in gross profit margin driven by restrained discounts and optimized product mix. Operating profit margin improved by 1.6pp YoY to 21.3%

Mainland China business saw sales growth across all product categories, led by Household goods and Food, resulting in significant growth of revenue and profit. In addition to strengthening local merchandising and marketing initiatives, small-scale renovations also contributed. LFL store + EC sales in Q3 (9 months) were 114.5% YoY.

Taiwan business saw increased revenue and profit, driven by strong sales of Household goods and Food, as well as an improvement in discount rate.

Hong Kong business saw improved profitability, leading to significant increase in both revenue and profit. In particular, Health & Beauty and Housewares drove sales growth.

Korea business saw significant revenue and profit growth due to implementation of product, marketing and operational initiatives.

Southeast Asia and Oceania business: Operating profit margin improved as SG&A/revenue ratio improved due to sales growth, resulting in a significant increase in operating profit.

Operating revenue was 49.0 billion yen (134.7% YoY) and operating profit was 6.9 billion yen (155.5% YoY).

Under a strengthened management structure, store environment improvements were accelerated and sales plans were reviewed.

LFL store + EC sales in Q3 (9 months) were 108.9% YoY.

Operating profit margin improved to 14.2% due to improved SG&A/revenue ratio accompanying sales growth.

LFL store + EC sales posted double-digit growth YoY in Thailand business, Malaysia business, Vietnam business and Australia business.

For Singapore business, while LFL store + EC sales decreased YoY due to price revisions and restrained discounts, profitability improved.

For the Philippines business, the first-ever MUJI Week has succeeded, and LFL store + EC sales increased YoY.

Europe and North America business: LFL store sales continued to perform well. Store openings resumed and investments for future growth began.

Operating revenue was 37.7 billion yen (121.9% YoY) and operating profit was 5.5 billion yen (103.8% YoY).

Operating revenue increased, driven by an expanded product lineup and growth in EC sales. LFL store + EC sales in Q3 (9 months) were 111.3% YoY.

Operating profit increased slightly. However, operating profit margin deteriorated due to higher expenses related to future growth, including store openings and logistics. The positive impact from foreign exchange also diminished.

For Europe business, both revenue and profit rose. LFL store + EC sales posted double-digit growth YoY. Additionally, EC sales grew significantly following the integration of EC platforms in Europe during FY25/8.

For North America business, revenue increased, driven by increase LFL store + EC sales. New storers in Cambridge, Boston and Queens, New York got off to a strong start. While operating profit increased on a local accounting basis, profit declined on segment basis as the positive impact of foreign exchange diminished. SG&A/revenue ratio deteriorated due to the incremental costs for transfer of logistics centers and resumption of store openings.

Number of Stores: 1,463 (Japan: 708, Overseas: 755)

For Japan business, the number of stores increased by 25 to 708 as we opened profitable stores mainly in suburbs.

For overseas business, the number of stores increased by 26 to 755.

For East Asia business, the number of stores increased by 17 to 574.

For mainland China business, the number of stores increased by 8 to 430. We continued to promote scrap and build strategy and small-scale renovations. We opened a large-scale store in Shanghai (over 2,800 ㎡).

For Southeast Asia and Oceania business, the number of stores increased by 8 to 132.

For Europe and North America business, the number of stores increased by 1 to 49.

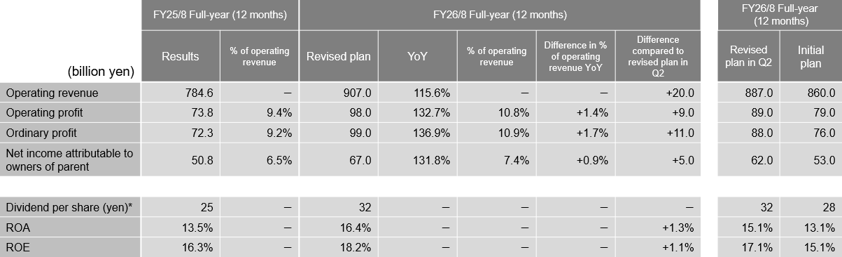

FY26/8 Full-Year Consolidated Plan: Upward revision for the second time this fiscal year reflecting primarily the results through Q3. Full-year operating profit and operating profit margin are expected to reach record highs.

Operating revenue has been revised upward by 15.6% YoY to 907.0 billion yen, mainly driven by strong performance in overseas business.

Operating profit has been revised upward by 32.7% YoY to 98.0 billion yen, mainly driven by Japan business and East Asia business. Expected to achieve the forecast for FY27/8 under 3 year rolling plan (FY26/8 – FY28/8) ahead of schedule.

Operating margin is expected to be 10.8%, driven by improvements in gross profit margin and SG&A/revenue ratio resulting from strong sales.

Net income attributable to owners of the parent is expected to be 67.0 billion yen, including one-time gains and losses, with ROE expected to reach 18.2%.

Foreign exchange rate plan for Q4 (3 months) remains unchanged. The impact related to the situation in the Middle East on this fiscal year’s performance is expected to be limited.